Release: 2026-2.49.0

Update: March 11, 2026

United States

Federal

HSA Catch-up - effective date March 11, 2026

A new flag, Use Catch-Up Contribution Limits (HSA), has been added to Employee Payroll Settings ~ Tax Settings. When enabled for employees age 55 or older, the system will apply the applicable 2026 HSA catch-up contribution limits:

- Single coverage: $5,300

- Family coverage: $9,550

American Samoa

State Unemployment Tax – effective January 1, 2026

As a result of an internal audit, the American Samoa State Unemployment Tax was deactivated. Although the territory does have a local income tax system, there is no separate territorial unemployment insurance program, and no SUTA is remitted.

Delaware

State Unemployment – effective January 1, 2026

The tax wage base increased from $12,500 to $14,500. The new employer rate remains 1.2% in 2026 pending any updates from the agency.

Training Tax – effective January 1, 2026

The tax rate decreased from 0.126% to 0.11%. Additionally, the wage base increased from $12,500 to $14,500.

Kentucky

Warsaw OLF – Effective January 1, 2026

The wage base increased from $176,100 to $184,500. The tax rate remains 1.75%.

Louisiana

Income Tax – effective January 1, 2026

The tax standard deductions were updated:

- Single or married filing separately: updated from $12,500 to $12,875

- Married filing jointly, qualifying surviving spouse, or head of household: updated from $25,000 to $25,750

The tax rate remains 3.09%.

Massachusetts

Income Tax – effective January 1, 2026

The tax personal exemption amount has increased from $5,800 to $5,900.

The tax rate remains 4.25%.

Paid Family and Medical Leave (PFML) – ACTION REQUIRED – effective March 11, 2026

We resolved an issue in which Massachusetts PFML taxable wages were erroneously doubled. This occurred when a benefit was configured with Affects Tax Calculation enabled, and the Impact on Taxable Wage under US Tax Settings was set to a value other than Per Calculation Engine, for example, when the configuration was explicitly including or excluding specific taxes.

Action Required

Please verify your Massachusetts PFML taxable wages — they should match your Massachusetts Unemployment taxable wages. Make any necessary adjustments to correct prior records.

State Unemployment – effective January 1, 2026

The new employer rate increased from 2.13% to 2.42%. The wage base remains $15,000.

Michigan

Benton Harbor City Tax – effective January 1, 2026

The Total Allowances miscellaneous parameter has been added to the Benton Harbor City Tax. When calculating taxable wages, the engine now subtracts $750 per allowance claimed from the employee’s annual income. For tax year 2026, the allowance value is $750.

Per agency guidance, the terms “allowances” and “exemptions” are used interchangeably.

Minnesota

Paid Family and Medical Leave (PFML) – ACTION REQUIRED – effective March 11, 2026

We resolved an issue in which Massachusetts PFML taxable wages were erroneously doubled. This occurred when a benefit was configured with Affects Tax Calculation enabled, and the Impact on Taxable Wage under US Tax Settings was set to a value other than Per Calculation Engine, for example, when the configuration was explicitly including or excluding specific taxes..

Action Required

Please verify your Minnesota PFML taxable wages — they should match your Minnesota Unemployment taxable wages. Make any necessary adjustments to correct prior records.

Paid Family and Medical Leave (PFML) – effective January 1, 2026

The default contribution percentage for a qualified small employer has been updated from 50 to 66.6667.

North Dakota

Income Tax – effective January 1, 2026

The tax brackets were updated for all filing statuses. The value of an annual allowance remains $5,050 and the supplemental rate remains 1.5%.

Northern Mariana Islands

State Unemployment Tax – effective January 1, 2026

As a result of an internal audit, the Northern Mariana Islands State Unemployment Tax was deactivated. Although the territory does have a wage and salary tax, there is no separate unemployment insurance program, and no SUTA is remitted.

Ohio

Berkshire Township JEDD I & JEDD II – effective January 1, 2024

Tax credits were updated to 50%, and the credit limits were updated to 0.925%.

College Corner City Tax – effective September 13, 2025

The tax was deactivated and is no longer in effect.

Delta City Tax – effective January 1, 1900

The tax credit was corrected from 66.67% to 100% effective January 1, 1900, to reflect the correct credit structure for all supported periods. The tax rate remains 1.5% and the credit remains 1% for 2026.

Gallipolis City Tax – effective January 1, 2026

The tax rate increased from 1% to 1.5% and the credit limit increased from 1% to 1.5%. The credit remains 100%.

Upper Sandusky City Tax – effective December 17, 2025

The tax rate increased from 1% to 1.75%. The credit and credit limit remain 0%.

Village of Indian Hill City Tax – effective January 1, 2026

The tax rate has increased from 0.45% to 0.5%. The credit and credit limit remain 0%.

Pennsylvania

Bethel Park, Bethel Park S D EIT– effective January 1, 2026

- The total resident EIT rate increased from 1.5% to 1.75%

- The municipal resident EIT rate has increased from 1% to 1.25%

- The school district resident EIT rate remains 0.5%

- The municipal nonresident EIT remains 0%

- The municipal low income exemption (LIE) remains $0

- The school district low income exemption (LIE) remains $0

Borough of Blain LST - West Perry School District – effective January 1, 2026

- The total LST amount increased from $0 to $52

- The municipal LST increased from $0 to $52

- The school district LST remains $0

- The municipal low income exemption (LIE) increased from $0 to $12,000

- The school district low income exemption (LIE) remains $0

Borough of Lanesboro, Susquehanna Community School District EIT

- The total resident EIT increased from 0% to 1%

- The municipal resident EIT rate has increased from 0% to 1%

- The school district resident EIT rate remains 0%

- The municipal nonresident EIT has increased from 0% to 1%

- The municipal low income exemption (LIE) remains $0

- The school district low income exemption (LIE) remains $0

Borough of Marianna LST - Bethlehem-Center School District – effective January 1, 2026

- The total LST amount increased from $10 to $15

- The municipal LST increased from $5 to $10

- The school district LST amount remains $5

- The municipal low income exemption (LIE) remains $0

- The school district low income exemption (LIE) remains $0

Bristol Township, Bristol Township S D EIT– effective January 1, 2026

- The total resident EIT rate remains 0.5%

- The municipal resident EIT rate remains 0.5%

- The school district resident EIT rate remains 0%

- The municipal nonresident EIT remains 0.5%

- The municipal low income exemption (LIE) decreased from $4,000 to $0

- The school district low income exemption (LIE) remains $0

City of Lancaster, Lampeter-Strasburg School District

- The total LST amount decreased from $52 to $47

- The municipal LST decreased from $52 to $47

- The school district LST remains $0

- The municipal low income exemption (LIE) remains $12,000

- The school district low income exemption (LIE) remains $0

Exeter Township, Wyoming Area School District LST - effective January 1, 2026

- The total LST amount increased from $10 to $30

- The municipal LST increased from $5 to $25

- The school district LST amount remains $5

- The municipal low income exemption (LIE) increased fro m0% to $12,000

- The school district low income exemption (LIE) remains $0

Middletown Township, Neshaminy School District EIT – effective January 1, 2026

- The total resident EIT increased from 0.5% to 1%

- The municipal resident EIT rate has increased from 0.5% to 1%

- The school district resident EIT rate remains 0%

- The municipal nonresident EIT has increased from 0.5% to 1%

- The municipal low income exemption (LIE) remains $12,000

- The school district low income exemption (LIE) remains $0

New Castle, New Castle Area S D EIT – effective January 1, 2026

- The total resident EIT rate remains 2.075%

- The municipal resident EIT rate remains 1.575%

- The school district resident EIT rate remains 0.5%

- The municipal nonresident EIT increased from 1.148% to 1.271%

- The municipal low income exemption (LIE) remains $0

- The school district low income exemption (LIE) remains $0

Pittston, Pittston Area S D EIT – effective January 1, 2026

- The total resident EIT rate increased from 2.2% to 2.7%

- The municipal resident EIT rate increased from 1.7% to 2.2%

- The school district resident EIT rate remains 0.5%

- The municipal nonresident EIT remains 1%

- The municipal low income exemption (LIE) remains $0

- The school district low income exemption (LIE) remains $0

Township of East Brunswick, Blue Mountain School District

- The total LST amount remains $10

- The municipal LST remains $5

- The school district LST amount remains $5

- The municipal low income exemption (LIE) increased from 0% to $12,000

- The school district low income exemption (LIE) remains $0

Upper Uwchlan Township, Downingtown Area School District LST – effective January 1, 2026

- The total LST amount increased from $10 to $52

- The municipal LST remains $42

- The school district LST increased from $0 to $42

- The municipal low income exemption (LIE) increased from $0 to $12,000

- The school district low income exemption (LIE) remains $500

Puerto Rico

Territory Income Tax – effective January 1, 2016

The tax amounts are rounded to the nearest cent rather than to the nearest whole dollar.

Based on confirmation from the Puerto Rico Department of Hacienda and a review of published guidance, there is no requirement to round withholding amounts to whole dollars. Additionally, the Developer Guide for Electronic Filing Requirements for Forms 499R-2/W-2PR explicitly instructs filers not to round. From page 18 of their guide: "DO NOT round to the nearest dollar".

State Unemployment Tax – effective January 1, 2026

The new employer rate decreased from 3.1% to 2.8%. The wage base remains $7,000.

Added a new parameter, Allow Zero Rate to Tax Maintenance ~ TAX CODES. When set to true the tax will be calculated at a tax rate of 0% when the Rate is set to 0.

Special Assessment Tax – effective January 1, 2026

Added a new parameter, Allow Zero Rate to Tax Maintenance ~ TAX CODES. When set to true the tax will be calculated at a tax rate of 0% when the Rate is set to 0.

North Dakota

Income Tax – effective January 1, 2026

The tax brackets were updated for all filing statuses. The value of an annual allowance remains $5,050 and the supplemental rate remains 1.5%.

Ohio

Berkshire Township JEDD I & JEDD II – effective January 1, 2024

Tax credits were updated to 50%, and the credit limits were updated to 0.925%.

We confirmed this change with the City of Delaware Income Tax Department directly.

College Corner City Tax – effective September 13, 2025

The tax was deactivated and is no longer in effect.

Delta City Tax – effective January 1, 1900

The tax credit was corrected from 66.67% to 100% effective January 1, 1900, to reflect the correct credit structure for all supported periods. The tax rate remains 1.5% and the credit remains 1% for 2026.

Village of Indian Hill City Tax – effective January 1, 2026

The tax rate has increased from 0.45% to 0.5%. The credit and credit limit remain 0%.

South Dakota

Administrative Fee -effective January 1, 2026

The rate increased from 0.02% to 0.08%. The wage base remains $15,000.

Virgin Islands

State Unemployment – effective January 1, 2026

Added a new parameter, Allow Zero Rate to Tax Maintenance ~ TAX CODES. When set to true the tax will be calculated at a tax rate of 0% when the Rate is set to 0.

West Virginia

Romney City & Smithers City Service Fees – effective July 1, 2015

The fees are exempt for residents. As a result, the resident tax rate was updated from 1% to 0% for the Romney City Service Fee.

Washington

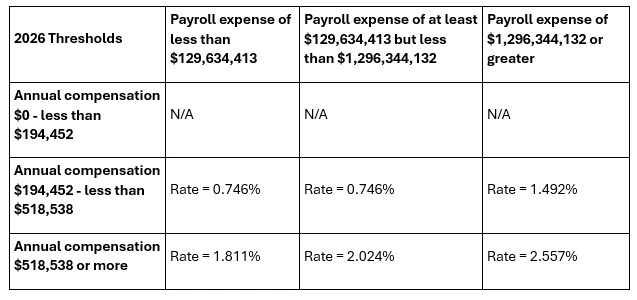

Seattle Payroll Expense Tax – Action Required – effective January 1, 2026

The tax rates and thresholds have been updated:

Action Required: Acumatica Payroll does not currently support Payroll Expense Tax; this tax must be calculated and filed manually.

West 11VirginiaRomney City & Smithers City Service Fees – effective July 1, 2015 The fees are exempt for residents. As a result, the resident tax rate was updated from 1% to 0% for the Romney City Service Fee. 26 Thresholds | Payroll expense of less than $129,634,413 | least $129,634,413 but less than $1,296,344,132 | Payroll expense of $1,296,344,132 or greater | ||

| Annual compensation $0 - less than $194,452 | N/A | N/A | N/A | ||

| Annual compensation $194,452 - less than $518,538 | Rate = 0.746% | Rate = 0.746% | Rate = 1.492% | ||

| Annual compensation $518,538 or more | Rate = 1.811% | Rate = 2.024% | Rate = 2.5 |