Please see attached for a list of 2024 Payroll tax updates. Please note that some changes may require an action to be utilized. They will be flagged with a Y in Action Required column.

Update: April 25, 2024

Canada

Federal Employment Insurance Tax – Effective 4/25/2024

A new field, Custom Employment Insurance tax rate, has been added to Tax Maintenance ~ Company Tax and to Employee Payroll Settings ~ Tax Settings to support EI Premium Reduction Program.

Optional: Employers that qualify can use this field to add the lower tax rate to be applied to the employer portion of the tax.

United States

Washington Paid Medical and Family Leave- Effective 4/25/2024

Corrected an issue where the taxable wage for Washington PFML was doubling on Government Reporting using the WA PMFL Form.

Update: April 5, 2024

United States – HSA – Action Required – Effective 3/19/24

The Federal HSA family contribution limit has changed from $8350 to $8300.

ACTION REQUIRED: Review employee HSA family contributions that may have exceeded the $8300 limit.

Alabama – Income Tax – Effective 1/1/24

Overtime wages earned in Washington DC by an Alabama resident are exempt from income tax.

Indiana – Income Tax – Effective 1/1/24

REVERTED: “Indiana will tax residents fully and will not provide credit for wages earned in another state.”

Indiana will continue to provide a tax credit for the tax paid to another state.

Iowa – Income Tax – Effective 2/23/24

The 2023 IA W-4 form and prior can still use the total allowances field. The engine will take the number of allowances and multiply by 40.

NOTE: Filing status is no longer used or supported. It was never used to calculate Iowa Income Tax.

Kentucky City, County or OLF – Action Required – Effective 3/8/2024

Corrected an issue where the subject wages could potentially exceed the wage base when the following conditions were all met:

1. The tax being calculated is a percentage-based Kentucky city or county OLF with a wage base

2. Both regular and supplemental wages have been set up.

3. The combined regular and supplemental wages are currently crossing the wage base

ACTION REQUIRED: Review Kentucky local taxable wages and taxable gross and adjust for any employee that may have been exposed to this issue.

Kentucky Campbell County Senior Citizen Tax – Effective 1/1/24

Corrected an issue that caused this tax to be missing from paychecks.

Kentucky Middlesboro OLF – Effective 4/1/24

The rate increased from 2% to 2.45%.

Kentucky West Buechel OLF – Action Required – Effective 1/1/24

Correction: The wage base does not have a limit. However, only $50,000 in tax can be collected.

ACTION REQUIRED: Review any employees in this local that may have exceeded $50,000 taxable wages and make corrections.

Oregon Quarterly Tax Report (OQ) showed the incorrect amounts for Taxable wages for Family Leave Insurance. The report has been corrected so that the correct amount displays.

ACTION REQUIRED: Review Quarter 1 2024 reports to ensure that the correct taxable wages show for Family Leave Insurance (FLI).

NOTE: As of January 1, 2024, FLI no longer follows Unemployment taxable wages but instead follows the Social Security Wage base.

Pennsylvania FSA – Effective 1/1/23

The taxability of Dependent Care FSA benefits has been updated for Pennsylvania State Tax. Both Employee and employer contributions are no longer subject to withholding tax.

Pennsylvania Homestead LST - Effective 1/1/24

The total LST amount increased from $40 to $52.

Page 1 / 1

@SoniaEchols90 Do you know if there are known issues with the April tax update regarding the US federal income tax withholding calculations. We’ve seen some employees withholdings change incorrectly after applying the tax update.

@SoniaEchols90 Do you know if there are known issues with the April tax update regarding the US federal income tax withholding calculations. We’ve seen some employees withholdings change incorrectly after applying the tax update.

Hi,

I am not aware of any issues. If you are not able to validate then please contact support.

Thank you,

Sonia

I just had the same thing reported. Client has salaried employees so taxable wages and and FIT are very consistent. They just performed Tax Maintenance and FIT tax dropped significantly. What is going on with the Tax Maintenance?

Paychecks with different withholding amounts are:

– Ref # 1509 – Previous FIT WH: $103.84 – New FIT WH: $131.54

– Ref # 1508 – Previous FIT WH: $405.52 – New FIT WH: $277.59

– Ref # 1510 – Previous FIT WH: $717.35 – New FIT WH: $549.56

– Ref # 1511 – Previous FIT WH: $275.36 – New FIT WH: $318.36

Hi Tammy,

Can you please open a case so that we can investigate?

Thank you,

Sonia

@SoniaEchols90 - I did Case #368907 was created a few minutes ago. FYI...I have another client reporting issues with FIT but this one indicates the FIT went up. I still need to research this one. I will create a case on it if I find the same situation.

Our customer is having the same issue. They are salaried and FIT went up. See case 369113

Just an update that we are actively looking into this issue. Impacted employee are using the 2020+ W4.

The issue has been resolved. We re-deployed the release and it is now working. Checks just need to be recalculated.

Update: 6/19/2024

We have transitioned from Symmetry's legacy Location Code Service (LCS) to Symmetry Location Service (SLS).Action Required

This is a new and improved geocoding Location Service.

NOTE: We have an application change that will be delivered in a future release before customers can reap the full benefit of the new service as described below.

With the SLS in place, the engine will be able to precisely identify the applicable taxes at a more granular local level. It returns more precise location codes allowing you to pinpoint additional tax jurisdictions that may exist inside (or partially inside) traditional city boundaries. Which will help resolve the determination of whether JEDDs and other local taxes are applicable/ subject to withholding.

Action Required:

Navigate toTax Maintenance (PR208000)

Update Taxes under Tax Maintenance (PR208000)

Assign Taxes to Employees

Navigate to Employee Payroll Settings (PR203000) ~ TAXES

Review tax setup of problematic employees with local taxes to ensure taxes are properly set up.

If the employee reached the First ceiling of wages and did not exceed the Second ceiling of wages for CPP/QPP then the subsequent payrolls did not collect the Second ceiling CPP/QPP amounts. A change has been made so that the Second ceiling CPP/QPP wages will be collected. However, with this solution the limit will not be respected, and amounts will continue to be collected unless you follow the steps below. A permanent solution will be delivered later this year.

ACTION REQUIRED: The workaround until the permanent solution is delivered is to store the YTD values of the Second ceiling in tax settings.

Run the Taxes by Employee(PR641067) report for Year: 2024 and Tax Code: CAN CPP. Do not check Include Unreleased.

Export to Excel.

Find any employees with YTD Tax Wages greater than $68,500. Take YTD Tax Wages less $68,500 to arrive at the employee’s Second Ceiling Wages YTD.

For example, an employee’s YTD Tax Wages are $71,175.01. $71,175.01 – $68,500 = $2,675.01

Next take YTD Tax Amount less $3,867.60 to arrive at the Second Ceiling Tax YTD.

For example, an employee’s YTD Tax is $3,974.50. $3,974.50 - $3,867.50 = $107

Navigate to Employee Payroll Settings (PR2030PL) ~ TAXES ~ CAN CPP for the employee.

In the YTD Second Additional CPP Tax Contribution enter the employee’s Second Ceiling Tax YTD.

For example, $107.

In the YTD Second Additional CPP Wage Contribution enter the employee’s Second Ceiling Wages YTD.

For example, $2,675.01

Calculate payroll as normal.

NOTE: You will need to do this for every payroll until the employee has reached the max tax and max taxable wages for the Second Ceiling and you have set YTD Second Additional CPP Tax Contributionto $188and the YTD Second Additional CPP Wage Contributionto $4700 under Employee Payroll Settings (PR2030PL) ~ TAXES ~ CAN CPP.

The same logic will be used for QPP. Please Note that the Max Tax for QPP is different from CPP, see table below. Also, the fields to be updated under Employee Payroll Settings (PR2030PL) TAXES ~ CAN QPP will be YTD Second Additional QPP Tax Contribution and YTD Second Additional QPP Wage Contribution.

NOTE: If an employee transferred mid-year to or from Quebec to or from another province then enter the YTD tax and Taxable Wages for the Frist Tier only. Use the Second Additional Transferring Into for the Second-Tier amounts.

For example, an employee transfers from Ontario to Quebec. They have $70,000 YTD CPP Taxable Wages and $3,927.50 YTD CPP Tax. Under Employee Payroll Settings (PR203000) ~ TAXES ~ CAN QPP Set:

CPP YTD Tax to 3867.50

CPP YTD wages to 68500

YTD Second Additional CPP Tax Contribution Transferring Into to 60

YTD Second Additional CPP Wage Contribution Transferring Int to 1500

2024

YMPE

Max Wages

basic

exemption

1st Ceiling

%

1st Ceiling

Max Tax

YAMPE

Second Ceiling

%

Second Ceiling

Max Tax

Total

Tax

Second Ceiling

Max Wages

CPP

68,500

3500

5.95%

3,867.50

73,200

4%

188

4,055.50

4700

QPP

68,500

3500

6.4%

4,160

73,200

4%

188

4,348

4,700

YMPE - Year’s Maximum Pensionable Earnings is set by the government every year in January based on increases in the average wage in Canada (First ceiling).

YAMPE - Amount of the second earnings ceiling starting in 2024. It will be 7% higher than the First ceiling.

Federal/Quebec Wage Type – Effective 6/19/2024

Corrected an issue that caused earnings to be incorrectly taxed when an Earnings Type Codes (PR102000)Wage Type: set to “Custom” and had a Taxability Setting of “Cash Non-Subject Non-Taxable for a Tax Code”.

United States

Federal HSA Effective – Effective 6/19/2024

When setting up a Deduction and Benefit Codes (PR101060) form with a Code Type: “HSA” under USTAX SETTINGS will now default with a Reporting Type: “Under Box12W - W - Company's Contribution to an Employee's Health Savings Account (HSA)” under EMPLOYER CONTRIBUTION. Previously, Reporting Type: under EMPLOYER CONTRIBUTION was defaulting to “Box12DD - DD - Cost of Employer-Sponsored Health Coverage”.

Optional: Review your set up of current HSA accounts to ensure Employer Contributions are correctly mapped to Box 12W on the Employee's W-2.

Federal Simple IRA - Effective 6/19/2024

Corrected SIMPLE IRA scenario involving year-to-date Section 125 contributions. Section 125 employee contribution amounts are automatically subtracted from compensation when calculating SIMPLE IRA employer contributions, but any year-to-date Section 125 employer contributions will now be correctly included in the calculation when Allow employer SIMPLE IRA contributions is checked.

Allow employer SIMPLE IRA contributions is found under Tax Maintenance (PR208000) ~ COMPANY TAX ~ FEDOR Employe Payroll Settings (PR203000) ~ TAX SETTINGS ~ FED.

Federal Simple IRA - Effective 6/19/2024

Added a new flag Use increased SIMPLE IRA limit to Tax Maintenance ~ Company Tax Data and to Employee Payroll Settings ~ TAX SETTINGS to support Secure Act 2.0. For 2024, there are new increased limits available. Employees participating in a SIMPLE IRA plan can use an increased deferral limit of $17,600 (i.e, a 10% on the $16,000 annual contribution limit) if the employer meets one of the follow conditions:

Employer has 25 or fewer employees receiving at least $5000 of compensation or

Employer has more than 25 but not more than 100 employees and makes either a 4% matching contribution or a 3% nonelective contribution.

NOTE: If the employer elects to make a 4% matching contribution, the employer contribution must be entered as a percentage rather than a flat amount.

All States Income Tax – Action Required - Effective 6/19/2024

Employees can be marked as exempt by selecting the Is Exempted Flag under Employee Payroll Settings ~ Taxes~ Tax Settings for the state SIT selected. We will be removing the flag Employee is exempt from state withholding under Employee Payroll Settings ~ Tax Settings in a future release.

Action Required: Ensure that employees exempt from a State Income tax are flagged as exempt using the Is Exempted flag under Employee Payroll Settings ~ Taxes~ Tax Settings for the state SIT.

Multi-State Calculations Income Tax – Effective 6/19/2024

Corrected a rounding issue that would occur in multi-state calculations when all the following conditions were met:

You are using the combined calculation method

The resident state is one of the following: Maine, Minnesota, Missouri, West Virginia

If Minnesota, then you must have set up the tax to either use default rounding or to always round (Minnesota recommends rounding, but it is not mandatory like the other three listed)

The nonresident work state is NOT returning a rounded result.

In this scenario, any credit from the nonresident state was applied after the rounding, causing the resident state to incorrectly return an unrounded tax amount. The credit will now be applied prior to the resident state tax getting rounded.

Kentucky, Corbin City OLF – Effective 6/19/2024

Corbin City exists both inside and outside of Whitley County. We have confirmed with the Whitley County Occupational Tax Administrator that Whitley County collects the occupational tax for the portion of the City of Corbin within its borders. Therefore, the Corbin OLF will now only be returned for the portion of the city outside of Whitley County.

Massachusetts Employer Medical Assistance Contribution (EMAC) - Effective 6/19/2024

On (Tax Maintenance (PR208000) ~ TAX CODES ~MA ER EMAC)

If the Override Wage Base miscellaneous parameter is NOT set:

The tax engine will now correctly obey the wage base and will stop withholding once crossed by the combined year-to-date wages and year-to-date employer benefit contributions to a 401(k) or Roth 401(k).

If the Override Wage Base miscellaneous parameter is set:

While the description for Override Wage Base states that is intended to be a "Year-to-date Subject Wages Override," it was previously acting like a gross wages override and was re-adding year-to-date employer benefit contributions to 401(k)s or Roth 401(k)s. The tax engine will no longer re-add these when Override Wage Base has been set.

Massachusetts Income Tax – Effective 1/1/2024

Massachusetts State Tax began calculating a 4% surtax on annual income over $1,053,750. Previously, this surtax could only be calculated on regular wages. With this release, we've added support for calculating this surtax on payrolls that only include supplemental (bonus) wages.

Calculations involving only regular wages, or involving both regular and supplemental wages, are unaffected by this update.

A new flag, Annual Wages has been added to support “flat” supplemental calculation method. When determining the surtax amount for flat supplement payrolls the tax engine will add current supplemental wages + Year-to-date supplemental wages + value set for Annual Wages.

Annual Wages flag is found under Tax Maintenance (PR208000) ~ COMPANY TAX ~ MA OR Employe Payroll Settings (PR203000) ~ TAX SETTINGS ~ MA.

Ohio Bellefontaine City Income Tax – Effective 7/1/2024

Rate increased from 1.333% to 1.6%.

Ohio Bucyrus City Income Tax – Effective 7/1/2024

Corrected tax credit from 100% to 88.89%

.

Ohio Coal Grove City Income Tax – Effective 6/4/2024

Added an address exception with the tax engine so that Coal City Grove City Tax was returned for 1238 County Road 24, Ironton, OH 45638

Ohio Coshocton City Income Tax – Effective 1/1/2016

Added with a rate of 1%. RITA will administer this tax.

Ohio Mercy West JEDD III Tax – Effective 10/1/2024

Rate decreased from 1.5% to 1%.

Ohio JEDD Tax – Effective 6/19/2024

Corrected potential for tax credit limit to be exceeded when an employee lives in one city and works in another city, and that work location is part of a JEDD, then the credit to the resident city was being applied for both the work city and the JEDD, causing the resident credit limit to be exceeded. Also, Resident City Tax Calculation Option is NOT set to None.

Resident City Tax Calculation Option is found under Tax Maintenance (PR20800) ~ COMPANY TAX ~OH OR Employe Payroll Settings (PR203000) ~ TAX SETTINGS~ OH.

Pennsylvania Income Tax Effective 6/19/2024

Corrected an intermittent issue with calculation results that could occur when you are running a calculation that involves two (or more) different Pennsylvania addresses that meet all of the following conditions:

The addresses result in the same location code

The addresses have different applicable EITs (due to different school districts within the same city, etc.)

The EITs have the same tax rate

Previously, the tax engine would return the withholding results under one of those EITs at random. Now, it will consistently use the correct EIT.

Vermont Child Care Contribution – Effective 7/1/2024

Support for Vermont's new Child Care Contribution (CCC) tax for both employees and employers has been added. The total tax is 0.44%, but employers can optionally elect to withhold up to 25 percent of the required contribution (i.e., 0.11%) from employee wages. The employer may choose to withhold a smaller portion of employee wages or choose not to withhold any amount from employees. Any input values greater than 0.11% for the Employee Percentage will cause the tax engine to use the maximum percentage of 0.11%. Unless specified otherwise, the tax engine will assume that the employer is not withholding any amount from employees (i.e., that the employer is paying the full 0.44% by default).

Employee Percentage flag is found under Tax Maintenance (PR208000) ~ TAX CODES ~ VT CCC OR Employe Payroll Settings (PR203000) ~ TAXES ~ VT CCC.

Virginia Income Tax - Effective 4/1/2024

The standard deduction amount increased from $8000 to $8500.

Washington Cares (LTI) - Effective 6/19/2024

Resolved an issue where WA Cares wages appear to be doubling the taxable wage using Government Reporting (PR504000) on WA PFML FORM.

Wisconsin Income Tax – Effective 1/1/2024

We've added support for Wisconsin's nonresident withholding threshold. No withholding will occur for a Wisconsin nonresident employee if their annual wages are less than the threshold.

Effective 1 January 2009, the Wisconsin State Tax nonresident minimum withholding threshold is $1,500.

Effective 1 January 2024, the Wisconsin State Tax nonresident minimum withholding threshold is $2,000.

The Wisconsin Department of Revenue has released the April 2024 Wisconsin Tax Bulletin which includes this withholding requirement threshold increase for nonresidents, retroactive to the beginning of the year.

Update: July 22, 2024

Canada

Federal Employment Insurance (EI) – effective July 22, 2024

Modified the Custom Employment Insurance Tax Rate from two digits to four digits pass the decimal place to increase precision.

United States

Georgia Income Tax - effective 7/1/2024

Flat tax rate decreased from 5.49% to 5.39%. Dependent allowance increased from $3,000 to $4,000.

Idaho Income Tax - effective 5/21/2024

The tax brackets for Single and Married persons have been updated. The annual withholding allowance increased from $4,534 to $3,600. The supplemental flat rate decreased from 5.8% to 5.695%.

Kentucky

Hardin County OLF - effective 7/22/2024

Hardin County will now return a $0 tax calculation whenever one of the following OLF has also been calculated: Elizabethtown OLF, Radcliff OLF, Vine Grove OLF and West Point OLF.

Grant County OLF - effective 7/1/2024

Rate increased from 1.5% to 2.5%

Bourbon County OLF – effective 7/1/2024

Rate increased from .75% to 1.25%

Flemingsburg OLF – effective 7/1/2024

Rate increased from .75% to 1.25%

Massachusetts

Workforce Training Fund – effective 1/1/2020

Employer contributions for 401(k) and Roth 401(k) will now be treated as taxable and will increase the subject wages.

COVID-19 Recovery Assessment – effective 1/1/2020

Employer contributions for 401(k) and Roth 401(k) will now be treated as taxable and will increase the subject wages.

Ohio

Income Tax – effective 7/1/2024

The rate for the top tax bracket (More than $100,000) has decreased from 4.41% to 3.8%.

Blanchester City Tax – effective 7/1/2024

Added with a rate of 1%, a credit factor of 100% and a credit rate of 1%. This tax is administered by RITA.

College Corner City – effective 7/1/2024

Added with a rate of 1%, no tax credit or credit limit. This tax is administered by RITA.

Glenmont City – effective 7/1/2024

Added with a rate of 1%, no tax credit or credit limit. This tax is administered by RITA.

Holmesville City – effective 7/1/2024

Added with a rate of 1%, no tax credit or credit limit. This tax is administered by RITA.

Louisville City – effective 1/1/2016

Credit rate updated from 1.2% to 2%

Mingo Junction City – effective 1/1/2023

Tax rate and credit rate decreased from 2% to 1%.

Perrysburg Toledo JEDZ – effective 1/1/2024

Deactivated as this tax is not collected through payroll withholding. Instead, the JEZ tax is allocated by the tax department of the City of Perrysburg from payments received from the Perrysburg City Tax, based on city records of business address that are subject to the JEDZ. Only businesses located within the city boundaries of Perrysburg are subject to the JEDZ.

The annual wage brackets for the employee CSPT have been updated.

Pennsylvania

Local Service Tax – effective 7/22/2024

Moved the Primary LST setting to be tax-specific instead of company and employee specific.

Antrim Township EIT – effective 7/1/2024

Nonresident rate decreased from .5% to 0%.

Dunkard Township LST – effective 7/1/2024

The municipal LST low-income exemption (LIE) amount increased from $0 to $12,000.

Duquesne City EIT – effective 7/1/2024

Resident rate decreased from 1.9% to 1%. Nonresident rate decreased from 1.4% to 1%.

Lincoln Township LST – effective 7/1/2024

Total LST amount increased from $5 to $10.

Northumberland Borough EIT – effective 7/1/2024

Resident rate increased from 1% to 1.45%.

Penn Township LST – effective 7/1/2024

Total LST amount increased from $5 to $10.

Petrolia Borough LST – effective 7/1/2024

Total LST amount decreased from $52 to $5.

Point Township EIT – effective 7/1/2024

Resident rate increased from 1% to 1.45%.

Rockefeller Township EIT – effective 7/1/2024

Resident rate increased from 1% to 1.45%.

Snydertown Borough EIT – effective 7/1/2024

Resident rate increased from 1% to 1.45%.

Sunbelt City EIT – effective 7/1/2024

Resident rate increased from 1% to 1.45%.

Upper Augusta Township EIT – effective 7/1/2024

Resident rate increased from 1% to 1.45%.

Utah Income Tax – effective 6/1/2024

Tax rate decreased from 4.65% to 4.55%. The value of a base allowance increased for Single ($440 from $415) and Married ($880 from $830). Amount subtracted from wages increased for Single ($8,8826 from $8,371) and Married ($17,652 from $16,742)

Complete list for 2024.

Update: August 29, 2024

Canada

Federal Employment Insurance (EI) – effective August 29, 2024

The code was corrected to ensure the calculation method is correctly set. Previously the EI was calculating too high.

United States

Arkansas

Arkansas Income Tax - effective dated July 1, 2024

The withholding formula has been updated. The supplemental tax rate decreased from 4.4% to 3.9%.

Arkansas Texarkana - effective date August 29, 2024

If an employee had Texarkana Resident checked and the employee lives in Texarkana TX but earns wages in Texarkana, AR the tax returned was always zero. Now this exemption can be turned off by unchecking Texarkana Resident for Texas. The employee wages will then be taxed in Arkansas.

District of Columbia Paid Family Leave – effective July 1, 2024

Employer rate increased from .26% to .75%

Hawaii Short Disability Insurance (SDI) – effective July 1, 2024

Corrected an issue when a single payroll run had both Regular and Supplemental wages and the premium cost was set to -1. Now the wages will be combined and the weekly wage base will be respected.

Indiana Allen County Income Tax – effective August 29, 2024

The Allen County Tax will now correctly treat employee contributions to a SIMPLE IRA as pre-tax for 2024, which means the contributions will reduce the subject wages for the tax.

This has always been the behavior for Allen County prior to April 2024, this fix restores the original intended behavior.

In addition, Allen County tax will now be collected when paying Supplemental wages. Previously, when calculating a Paycheck (PR302000) that has Supplemental earnings for a work location in Allen County of Indiana state, the Taxable Supplemental Wage of the location was incorrect.

Kansas Income Tax – effective July 1, 2024

Annual allowance has increased from $2.250 to $2,320. Tax brackets and personal allowances have been updated.

Kentucky Hurstbourne Acres OLF – effective July 1, 2024

New tax with a rate of 1%.

Note: Hurstbourne Acres - OLF has "stacked" taxes with the Louisville / Jefferson County - OLF.

Massachusetts Income Tax – effective July 1, 2024

Corrected an issue if a Full Time Student had supplemental wages. If the employee is marked as a full-time student, now their supplemental wages will be correctly treated as exempt.

Ohio

Mansfield City Income tax – effective January 1, 2025

Tax rate for resident and nonresident increased from 2% to 2.25%.

Village of Indian Hill Income Tax – effective January 1, 2024

Resident tax rate decreased from .475% to .45%.

Oregon

Income Tax – effective August 29, 2024

The state income tax withholding formula for Oregon uses the federal tax withheld as part of the withholding calculation (Oregon State Income Tax Withholding). There was previously an issue in multi-state scenarios with Oregon only when the Oregon regular wages didn't match the federal regular wages. The Oregen Wages instead of federal wages to calculate the FIT amount that is used as the deduction to the Oregon SIT calculation. Now the actual regular FIT tax amount will be used as the federal deduction amount for Oregon SIT (which means the deduction will decrease, which then increases the calculated tax)

Corbin City OLF – effective August 29, 2024

When both Whitley and Corbin City OLF taxes were set for an employee then taxes were returned only if there was a calculated amount. Going forward both will be returned even if the tax amount is zero.

Multnomah County Preschool Tax – effective August 29, 2024

If an employee is subject to Multnomah County tax withholding under the withholding calculation above, supplemental payments must have withholding applied. Income above $200,000 and below $400,000 must be withheld at a rate of 1.5% and income above $400,000 must be withheld at a rate of 3%.

Previously, the entire bonus amount would be calculated using the highest applicable rate. Now, the correct rate will be applied for the portions over and under the threshold(s).

Pennsylvania Petrolia Borough LST – effective July 1, 2024

LST amount increased from $5 to $52.

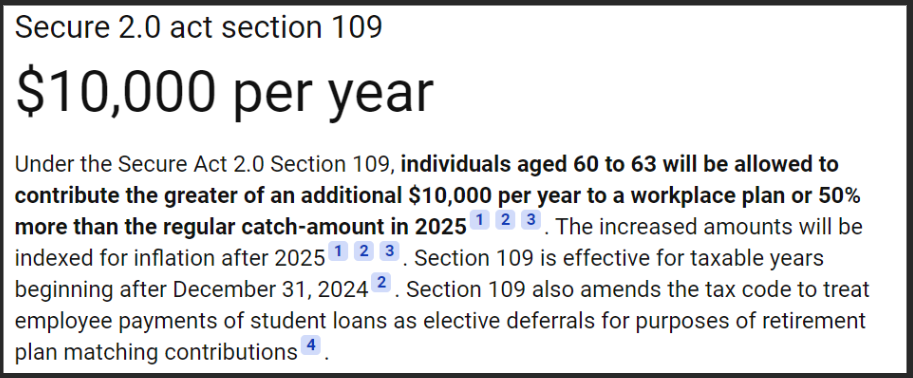

Our customer has adopted the Secure 2.0 Act Section 109 provisions related to catch-up contributions for employees aged 60-63 that is going into effect January 1, 2025. They have a large number of employees and will need to plan ahead for making changes to the employees’ tax settings. Will the options to “Use increased SIMPLE IRA limit” or “Use Catch-Up Contributions Limits” cover the changes for January or is there another setting they will need to have in place before January 1st?

@cbittle - I checked on this with our tax engine provider. Yes, they are aware of this need. Change will be coming in the future.

Calculation methods were not being honored if setup to use another method other than the default calculation method. Going forward, the tax methods selected will be utilized.

ACTION REQUIRED: Review the setup of Calculation methods under Tax Maintenance ~ TAX CODES (PR208000). Any employee that does not follow the default set for your company should be reviewed as well under Employee Payroll Settings ~ TAXES (PR203000). Below are the possible calculation methods: XX CAN PIT applies to BC, MB, NB, NL, NS, ON, PE, QC, SK and YT provinces\territories. Note: Commission/Draw is not available for QC Income Tax.

Annualized - This method multiplies the wages in the current pay period by the number of pay periods in a year to approximate total annual wages. Tax is calculated on the total annual wages. This amount is divided by the number of pay periods in a year to determine the tax for the current pay period.

Annualized Concurrent Aggregation - This method for determining the tax on Supplemental Pay is like the Concurrent Aggregation method, except that the Supplemental Pay amount is not annualized prior to being added to the annualized Regular Pay amount. The tax is calculated on the total amount of wages.

Annualized Previous Aggregation - This method is like the Previous Aggregation method, except that supplemental wages are not annualized prior to being added to the annualized Regular Pay amount.

This method combines the annualized Regular Pay amount from the previous pay period and the Supplemental Pay amount. Tax is calculated on this total amount. The amount of the tax paid on the previous Regular Pay wages is subtracted from the total. The result is the tax amount on the Supplemental Pay.

Commissions and Draws - This method is used for Federal and Provincial (except Quebec) calculations for an employee paid by commission.

Concurrent Aggregation - This method combines the Regular Pay with the Supplemental Pay into a total amount. Taxes are calculated on this total amount.

Cumulative - This method is used when wage amounts fluctuate over a range of pay periods. This method divides the sum of the current wages plus the Year-to-Date wages by the number of pay periods to date to compute an average wage for a given pay period. The tax is computed on the average wage as if this amount were paid to the employee each pay period. The taxes paid on Year-to-Date wages are subtracted from the tax on the average wages to determine the tax amount for the current pay period.

Cumulative Aggregation - This method combines the current wages and Year-to-Date wage amount to determine an average pay period wage. Tax is calculated on the average amount and multiplied by the number of pay periods so far, including the current pay period. The tax calculated is subtracted from the Year-to-Date tax amount that was already deducted. The current tax represents the amount to withhold for the current period.

Flat Rate - This method multiplies the current wage amount for the current pay period by a flat percentage.

Flat Rate Combined - This method multiplies the Supplemental Pay amount for the current pay period by a flat percentage. The tax on the Regular Pay is calculated using the annualized method. The total tax is the sum of these two calculations.

Flat Amount - This method applies a state-specified flat amount to a range of taxable gross wages.

Lump Sum - This method is used when an employee receives a special payment as defined in Canada Revenue Publication T4001. Taxes are calculated at a flat percentage rate.

No Self-Adjust - This method compares the Year-to-Date wages against the maximum wage limit specified for the jurisdiction. No adjustment is made if an employee has not paid sufficient taxes to date.

Previous Aggregation - This method combines regular wages from the previous pay period and the current supplemental wages. Taxes are calculated on this total amount. The amount of the tax paid on the previous Regular Pay wages is subtracted from the total. The result is the tax amount on the Supplemental Pay.

Self-Adjust -This method compares the Year-to-Date wages against the wage limit specified for the jurisdiction. Vertex Payroll Tax also checks the Year-to-Date tax amounts paid. An adjustment is made, if necessary, to "catch up" on an employee's taxes. After a wage limit is reached, no additional taxes are calculated.

Self-Adjust at Maximum - This method performs the same calculation as a Self-Adjust method when the employee's Year-To-Date gross has reached the maximum wage base. After a maximum wage base is reached, no taxes are withheld.

Note: The no self-adjust method is used prior to the maximum wage being reached.

Blank fields for the TD1 will now send a null value instead of a zero when paychecks are calculated. This could cause a change in the tax collected.

ACTION REQUIRED: Depending on the needs of your employees update Tax Maintenance ~ Company Settings (PR208000) by searching on Total Claim Amount under the Name column and set the default to blank, zero or the minimum personal claim amount. If Total Claim Amount is blank, it will use the basic personal amount in effect for that year as defined on Payroll Deductions Online Calculator - Canada.ca. If you choose to use blank, then the field cannot be marked as required. Then verify for employees that should only have the basic personal amount are set to default on Employee Payroll Settings ~ TAX SETTINGS (PR203000).

Each employee should fill out a TD1 for Federal and One for Province of Employment when hired or have a life change that impacts taxable wages. If the employee’s Province of Employment is Quebec, then they will fill out the TP-1015.3-V. Personal tax credits will be on line 10. Information from the employee's TD1(s)/TP-1015.3-V must be set up for each employee under Employee Payroll Settings ~ TAX SETTINGS (PR203000).

If an individual does not give the completed TD1 form, the individual's tax deductions should only include the basic personal amount you estimated based on their income.

If the employee has more than one employer, then they can only claim them for one employer at a time and should enter 0 in line 13. TOTAL CLAIM AMOUNT of the TD1 form.

Two new boxes have been added to the 2024 T4: Box 94 -Indian (exempt employment Income) - RPP contributions and Box 95 - Indian (exempt employment income) Union dues.

ACTION REQUIRED: (If applicable)

Setup up new deductions under Deduction and Benefit Codes (PR101060) screen to support First Nation employees T4 reporting of RPP contributions and/or Union dues associated with (exempt employment Income) and map the Federal Reporting type to Box 94 and/or Box 95.

Adjust prior 2024 deductions for RPP and Union Dues for 2024 for any earnings mapped to Box 71 - Indian (exempt employment income) to the new deduction code(s) so that they report in the appropriate boxes on the T4.

NOTE: An application change is needed also for this solution, it will be delivered later with other Year End items.

Update: October 21, 2024

Canada –

Canada – T4 – 10/21/24

Corrected an issue with the letter ‘P’ randomly appearing in box 28 instead of a check mark.